.png?width=711&name=Untitled%20design%20(10).png)

The size of the UK general insurance market has remained largely flat over the past few years and in a relatively static market, it is clear that policy growth for individual brands must primarily come from taking market share from other brands whilst maximising the retention of existing customers.

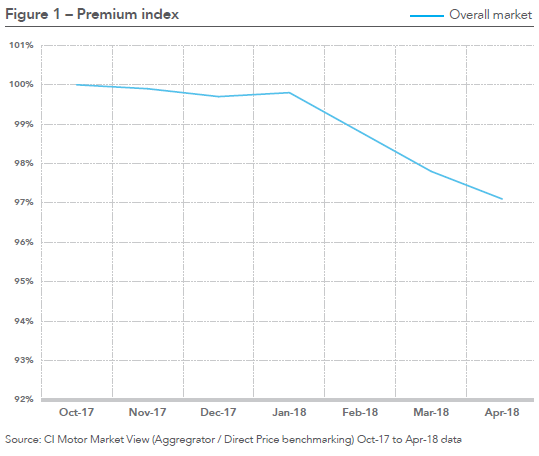

The motor insurance market is also currently in a period of premium deflation, putting further pressure on margins and increasing the commercial importance of retaining customers as demonstrated in Figure 1.

At the same time, with the FCA actively supporting customer shopping behaviour, customers are arguably being encouraged not to remain loyal to their brand for long periods of time.

On average however, most customers do not switch their insurance every year, even if they have shopped around.

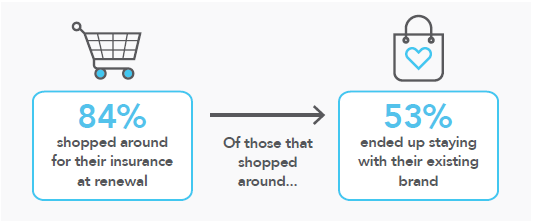

Data from Consumer Intelligence demonstrates that across motor insurance in 2017, around 84% of customers shopped around for their insurance at renewal. Of these 84% who shopped, 53% ended up staying with their existing brand. Given the costs of new customer acquisition, retention of customers remains extremely important. With a cost of acquisition per customer at around £100, it is simple arithmetic to identify that it is more profitable to keep a customer than to lose them and replace them with a new one.

Rajeev Aggarwal, Managing Director of Consumer Intelligence’s Advisory service commented:

“Of course, it is important in the very first place that brands acquire the ‘right’ type of customer for them. ‘Right’ in the sense of being within their risk appetite, underwriting footprint, ability to service and with appropriate levels of cover.”

Opportunities to maximise customer retention

Brands have several opportunities to maximise customer retention starting from the moment of initial acquisition and continuing through every customer touch point and communication (including mid-term adjustment, up- or cross-sell activity or claims) and culminating in the renewal activity itself.

It is inevitable that having acquired a customer in year one, a brand will lose some customers at the point of renewal, not least because of marketing/ product/price promotion activity from other insurance brands.

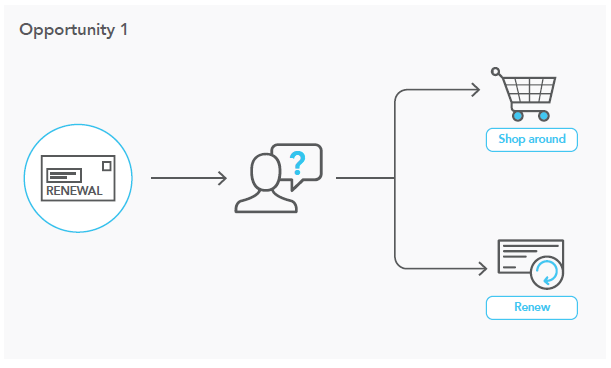

From a customer’s perspective, the primary ‘trigger’ in starting to decide whether to switch or stay is often the renewal invitation from the brand.

The creation of the renewal invitation is the first of two opportunities for an insurance brand to maximise

retention.

The sending of the renewal invitation will result in one of two actions from the customer:

- Begin the process of shopping around

- Decide not to shop around and just renew

Therefore, the brand who persuades more of their customers to take action point 2 has a benefit over its competitors who has more customers initially choosing action point 1.

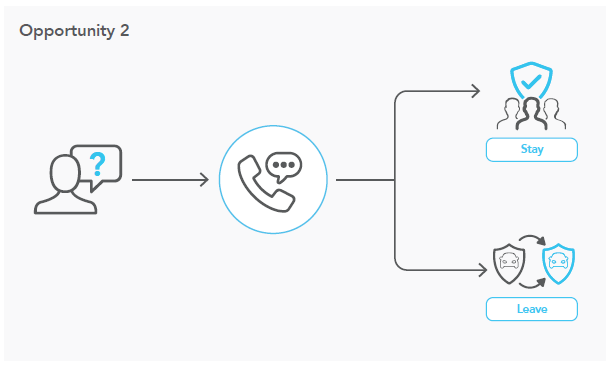

The second chance is to persuade those customers that have decided to shop around not to leave.

The recognition of the importance of this second chance to retain a customer is of course the reason for the creation by many brands of a dedicated customer insurance retention team. If a customer contacts the insurer with the intention of leaving, they are often diverted to a specialist team who will try and persuade the customer to stay, often through the negotiation of the renewal price. And ultimately the customer decides to stay or leave.

Generating profitable growth through customer retention

With the overall size of the UK general insurance market remaining relatively flat over the past few years, insurers recognise that growth for individual brands must primarily come from taking market share from other brands whilst maximising the retention of their existing customer base.

Using unique insights from our Insurance Behaviour Tracker (IBT), Consumer Intelligence has been able to determine that profitable growth is driven by a focus on renewals and that there is a proven link between brands with strong retention rates and high levels of customer engagement.

Comment . . .

Submit a comment